It might be difficult for consumers, and especially for those involved in sophisticated credit card processing systems, to understand how business got done before credit cards became a pervasive part of life. Of course, this pre-credit card period in history occurred before the internet. Nobody had to worry about safe online payments because ecommerce did not yet exist.

Even now, older generations will probably remember paying for a lot more goods and services with cash and checks in the past, but the concept of credit cards has actually been around for a long time. Certainly, the idea of credit existed for centuries, but it was more associated with specific merchants, unusually large purchases or businesses.

A Short Prehistory of Credit Cards

According to Credit Cards and Payment Efficiency, written for the Federal Reserve, almost all consumer and business purchases were paid with cash and checks during the early to middle part of the 20th century. Some of the first developments that paved the way towards modern credit cards include:

- Proprietary store charge cards: Early 20th century

- Gasoline cards: The 1920s

- Entertainment and travel cards: The 1950s

- Early bank cards: Late 1940s to 1950s

Proprietary Charge Cards

By the early 1900s, and even the late 1800s, some stores might issue charge cards, coins or tokens for customers to use only in that specific business. These were mostly processed manually, and debt was tracked in a paper ledger. Some larger stores did have a sort of press machine that made an imprint of a charge plate or token, but this still did not really qualify as automated processing.

The first proprietary store cards in the early 20th century did not represent revolving credit as debts were due at the end of the billing month. In fact, some stores hired companies that collected overdue debts by parking in front of customer’s doors with trucks or wagons that had very striking painting on the side, clearly marking them as debt collectors. Since neighbors could see these trucks, embarrassment seemed to be the primary method of enforcing timely payments.

Service Station Gasoline Cards

Service Station Gasoline Cards

In the early 1920s, oil companies issued paper courtesy cards to vehicle owners to encourage brand loyalty; this may have been the origin of consumer revolving credit. These were usually limited to a specific brand and even to a specific geographic area, so they couldn’t be used for traveling.

Travel and Entertainment Cards

By the 1950s, more general travel and entertainment cards appeared. Diners Club introduced their card in 1950, and it was the first time that consumers could really use their credit card outside of their own local area, and with any merchant who accepted the cards. American Express issued a similar travel and entertainment card called the “Green Card” in 1958. The bills still came due at the end of the payment period, so these did not represent true revolving credit.

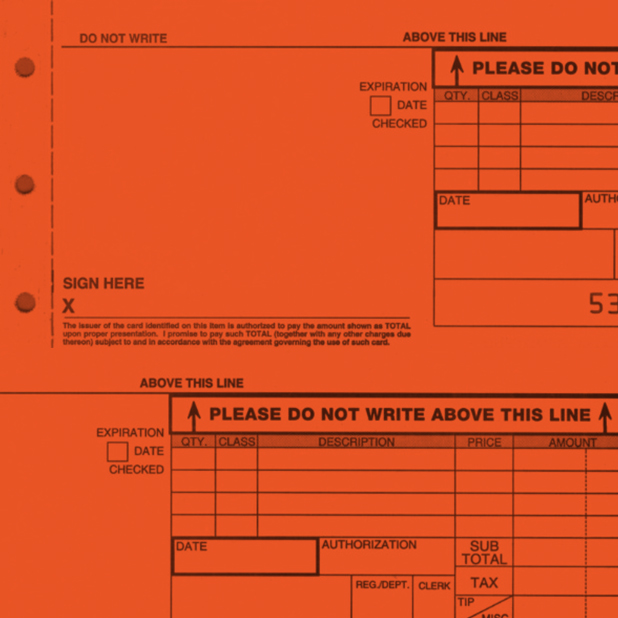

These were also handled very differently than the merchant services that businesses rely upon today. For one thing, it was a “closed loop” system where only the card issuer settled accounts with both consumers and merchants. Also, electronic POS systems did not exist, so all transactions got documented with paper forms and copies that had to be sent to the credit card company for processing. Security was still an issue because these paper forms could get lost, forged or have totals changed during processing.

These were also handled very differently than the merchant services that businesses rely upon today. For one thing, it was a “closed loop” system where only the card issuer settled accounts with both consumers and merchants. Also, electronic POS systems did not exist, so all transactions got documented with paper forms and copies that had to be sent to the credit card company for processing. Security was still an issue because these paper forms could get lost, forged or have totals changed during processing.

Early Bank Cards

In the latter part of the 1940s to the 1950s, some banks began issuing their own cards. Typically, cardholders had to have an account with the bank. Also, merchants had to sign up with each individual bank in order to accept the cards, and these were also usually only accepted within the limited geographic region that the bank served.

The Future of Credit Card Processing and Mobile Merchant Accounts

At Abtek, we have worked on the cutting edge of worldwide credit card processing technology since 1986. If you value security, integration and reliability, partner with us as your credit card processing solution of the future. We combine the latest in technology with old-fashioned customer service to deliver value for our merchant partners.

Read more in this series:

â‹… The History of Credit Cards, Part 2: Processing Before eCommerce

â‹… The History of Credit Cards, Part 3: The Evolution of True Digital Credit Card Systems

Share and Enjoy

If you’ve ever had to manually key a credit card number into an automated phone system, you’ve probably wondered why the number is so long. Actually, each digit in a credit card number is important for validation, security and identification during credit card processing. Take a moment to learn what each of these digits means.

If you’ve ever had to manually key a credit card number into an automated phone system, you’ve probably wondered why the number is so long. Actually, each digit in a credit card number is important for validation, security and identification during credit card processing. Take a moment to learn what each of these digits means.

In some cases, the system might request a PIN number, but this is usually only for very large purchases or in cases where the automated system detects unusual payment activity for a specific customer.

In some cases, the system might request a PIN number, but this is usually only for very large purchases or in cases where the automated system detects unusual payment activity for a specific customer.

In the 1930s and 40s, some stores issued charge plates to customers, perhaps the first example of semi-automated processing. These were simply small metal plates with a customer’s name and address engraved on the face. When a customer wanted to use their credit plate to make a purchase, a store employee would run it through a small machine that used an inked ribbon, sort of like an old typewriter ribbon, to make an impression on a sales slip with carbon copies.

In the 1930s and 40s, some stores issued charge plates to customers, perhaps the first example of semi-automated processing. These were simply small metal plates with a customer’s name and address engraved on the face. When a customer wanted to use their credit plate to make a purchase, a store employee would run it through a small machine that used an inked ribbon, sort of like an old typewriter ribbon, to make an impression on a sales slip with carbon copies.