The holiday season has once again come to an end. Whether your customers used in-store credit card processing systems or visited your ecommerce site, you don’t want to see your holiday profits whittled away by subsequent chargebacks.

Common Reasons for Chargebacks

Before we discuss how to prevent chargebacks, let’s look at the most common reasons that chargebacks occur.

- Fraudulent card was used

- Cardholder disputes merchandise quality

- Incorrect amount was charged to the card

- Errors occurred during credit card processing

- Proper authorization wasn’t obtained

General Prevention Tips

General Prevention Tips

Here are some general chargeback prevention tips that apply to merchants who accept online payments as well as swipe cards on POS systems.

- Be sure the customer recognizes the business name you give to your merchant services company. Many chargebacks occur because customers don’t recognize the business name that appears on their statement.

- Respond to retrieval requests in a timely manner. If you don’t respond within the number of days allowed in your merchant services agreement, it’s likely a chargeback will occur.

- Get an authorization 100 percent of the time. Failure to get an authorization will result a chargeback.

Prevention Tips for Swiped Cards

Prevention Tips for Swiped Cards

Following are tips that merchants who process cards through POS systems or mobile merchant accounts can follow to lessen the chance of a chargeback occurring.

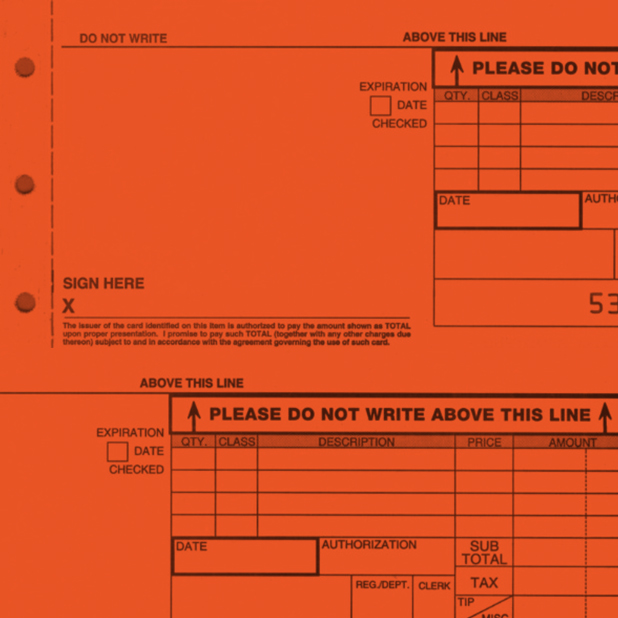

- Swipe all cards through your credit card processing terminal. Doing so proves the card was presented at your store. If you have to get an imprint because your terminal is down, be sure all information appears: amount, business name, business location and signature.

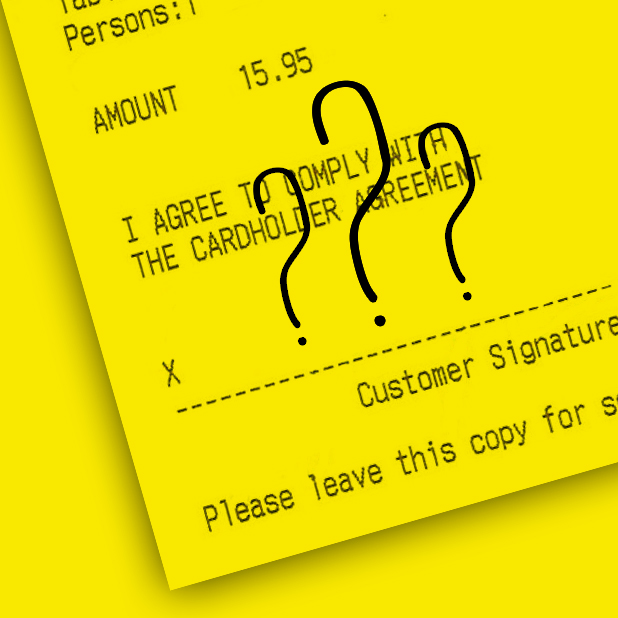

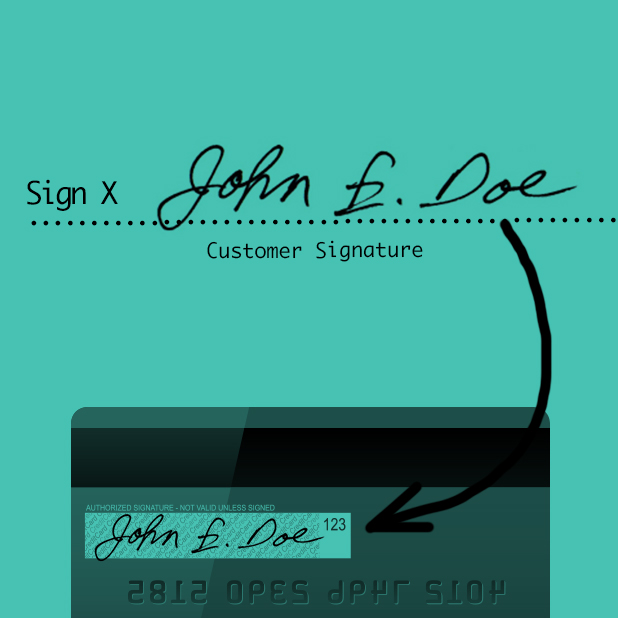

- Always compare the signature to the back of the card. Understandably your cashiers want to get customers through their lines quickly, but it only takes a few extra seconds to check the signature. Your cashiers should check the signature against a photo ID if there’s no signature on the back of the card.

- Ask for another form of payment if the card is declined. Don’t continue to swipe the card.

- Make sure the number on the screen and the credit card number match.

- Get an authorization for the full sale amount – don’t break the sale amount into smaller amounts.

Prevention Tips for Online Businesses

Prevention Tips for Online Businesses

Here are some helpful tips that online merchants can follow to prevent chargebacks.

- Make sure your customer is giving you the correct billing address by using the Address Verification System (AVS).

- Provide your merchant services company with a telephone number that it can print on your billing statement. This increases the likelihood that the customer will call you and determine what the purchase is before disputing it with their card issuer.

- Use shippers that provide proof of merchandise delivery to the full billing address. This will help you in case of a dispute. Require a signature for expensive merchandise to be left with the purchaser.

Stay up-to-date on payment processing trends by following Abtek on Twitter and Facebook. Sign up to receive our newsletter, too.

In some cases, the system might request a PIN number, but this is usually only for very large purchases or in cases where the automated system detects unusual payment activity for a specific customer.

In some cases, the system might request a PIN number, but this is usually only for very large purchases or in cases where the automated system detects unusual payment activity for a specific customer.

In the 1930s and 40s, some stores issued charge plates to customers, perhaps the first example of semi-automated processing. These were simply small metal plates with a customer’s name and address engraved on the face. When a customer wanted to use their credit plate to make a purchase, a store employee would run it through a small machine that used an inked ribbon, sort of like an old typewriter ribbon, to make an impression on a sales slip with carbon copies.

In the 1930s and 40s, some stores issued charge plates to customers, perhaps the first example of semi-automated processing. These were simply small metal plates with a customer’s name and address engraved on the face. When a customer wanted to use their credit plate to make a purchase, a store employee would run it through a small machine that used an inked ribbon, sort of like an old typewriter ribbon, to make an impression on a sales slip with carbon copies.