Payment aggregators or merchant aggregators provide services through which ecommerce businesses can process payment transactions. These service providers allow businesses to accept bank transfers and credit card payments without opening and maintaining a merchant account with a card association or bank. The aggregator facilitates the payment from a consumer via bank transfers, credit cards or stored value accounts to the merchant. Thus, the aggregator pays the merchant, not the consumer. These services have become increasingly popular, although they have downsides when compared to a traditional merchant services provider such as a bank. These include:

- Limitations to transaction size.

- Lack of PCI Compliance.

- Fewer filters to prevent fraud.

In general, payment aggregators hold consumer credit card data for quicker purchases, or they hold money for making future purchases. Companies such as Google Checkout, PayPal and Amazon Payments differ in their POS systems, credit card processing, services and costs for their merchant services. While these alternative merchant services have aggressively worked to establish themselves as market leaders, each business must assess the risks and analyze the costs in relation to traditional credit card processing to obtain the appropriate payment solution.

Transaction Limitations

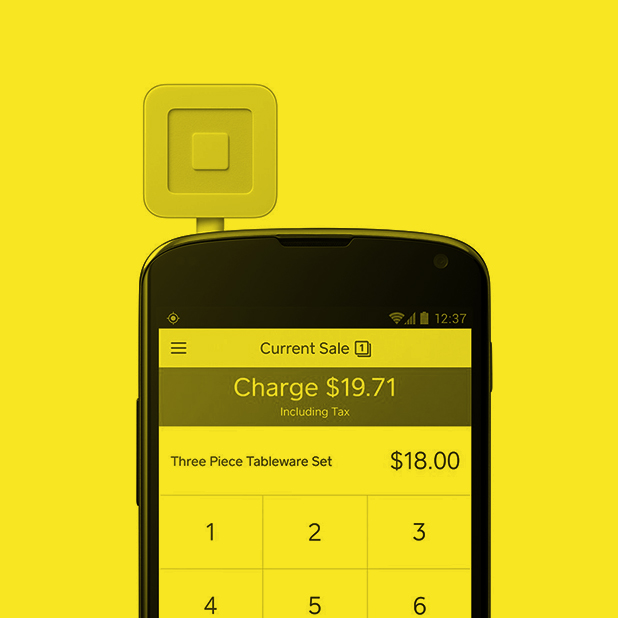

For instance, a business that sells high-end goods, may suffer from  lost sales because the credit card brands place an $8,000 limit per business per month. This limits online payments to lower priced goods. Moreover, as the service providers accept liability and risk for each transaction through the master account, individual transactions face maximum limits as well. Currently, the increasingly popular POS systems such as Square use an aggregator model that limits transactions to no more than $400. If a business exceeds those maximums, the automated system places holds on transactions up to 30 days, and those transactions may be subject to higher processing charges. Thus, two major drawbacks include:

lost sales because the credit card brands place an $8,000 limit per business per month. This limits online payments to lower priced goods. Moreover, as the service providers accept liability and risk for each transaction through the master account, individual transactions face maximum limits as well. Currently, the increasingly popular POS systems such as Square use an aggregator model that limits transactions to no more than $400. If a business exceeds those maximums, the automated system places holds on transactions up to 30 days, and those transactions may be subject to higher processing charges. Thus, two major drawbacks include:

- The money is not yours. Your business receives payment from the aggregator. The money collected from bank transfers or payment card transactions are property of the aggregator. If you violate the terms of agreement, the money may be held indefinitely.

- Higher fees for higher volume. After monthly volume exceeds certain levels, the fees can increase.

PCI Compliance

Another way that traditional merchant bank accounts provide safer credit card processing involves PCI compliance. Currently, all bank credit cards must follow PCI procedures to reduce liability and risk for the merchants for all account types. Most payment aggregators include that critical information only in the ultra-fine print. The merchants remain obligated to maintain PCI compliance despite using a payment aggregator that lacks the ability to screen for potential fraud. This applies to mobile merchant accounts as well.

If you do not maintain PCI compliance, you put your business at greater risk for the increasing threat of debit and credit card theft and data breaches, which could result in large fines from regulatory agencies, banks or card organizations, as well as lost customers and legal expenses.

greater risk for the increasing threat of debit and credit card theft and data breaches, which could result in large fines from regulatory agencies, banks or card organizations, as well as lost customers and legal expenses.

Thus, a small to medium sized entrepreneur faces higher risks when using POS systems like Square or aggregators such as Groupon for processing debit and credit card transactions. Traditional merchant accounts do not vary the liability and risks assumed based on processing volume, whereas many aggregators do. Smaller volume translates to higher risk ratios, which can lead to frozen funds and transactions in an automated system without regard for your cash flow needs. Moreover, without appropriate fraud screening methods to prevent risky transactions, the aggregators play catch up to the schemers at your expense.

Additional Costs

Lastly, it pays to investigate all of the potential costs for the  alternative payment methods. Many can be significantly higher than direct card payments. Further, costs may increase from fewer fraud guarantees and clearly defined processes for disputes. Fraudulent chargebacks may increase without any restitution from the service provider. Thus, while it may be tempting to take the easier, shorter route to accepting payments, a traditional merchant bank account offers better safety, lower risks and potentially higher profits.

alternative payment methods. Many can be significantly higher than direct card payments. Further, costs may increase from fewer fraud guarantees and clearly defined processes for disputes. Fraudulent chargebacks may increase without any restitution from the service provider. Thus, while it may be tempting to take the easier, shorter route to accepting payments, a traditional merchant bank account offers better safety, lower risks and potentially higher profits.

Read more in this series:

– Aggregators vs Merchant Banks, Part 2: The Costs of Payment Aggregators Adds up