The internet is currently abuzz about CurrentC. So what do you need to know about it, besides the fact that it’s clearly a play on words (“currency”)? Here are simply 10 facts.

• CurrentC is a proprietary QR code-based system developed by the Merchant Customer Exchange consortium–which includes these retailers.Â

• Some retailers include Dunkin’ Donuts, Wal-Mart, Best Buy, CVS, and 7-11.

• In this system, the QR code is referred to as a Paycode and it plays a pivotal role in how payments are scanned and processed.

• As a result, CurrentC does not feature NFC technolgy.

• Actually, not having NFC technology–in addition to requiring information such as a user’s social security number and driver’s license number–does not bode well for the payments system.

• From Business Insider also comes a description of how CurrentC. vs. Apple Pay vs. a traditional swipe:

Here’s how it works: When it’s time to pay for something, you get a QR code served to you on a payment terminal. You then open your phone, open the CurrentC app, then scan the QR code to pay. It can also work in reverse, where you open your phone, and you have a QR code, and the retailer scans the code.

Compare that with Apple Pay, which works like this: When it’s time to pay, take out your phone, hold it to the payment terminal, then use the phone’s fingerprint scanner to pay, and you’re done.

Or, compare both with credit cards: When it’s time to pay, take out your credit card, swipe it, sign, and be on your way.

• Even though Apple Pay can seem a little convoluted when it comes to user experience–it is integrated into an existing customer payment flow–whereas CurrentC complicates it.

• Many iPhone and Android fans from Reddit have converged on Twitter under the #PayItSafe hashtag to spread awareness about the dangers of mobile payments technology that lacks NFC.

• Which is all to say that if you’re a business that wants to minimize the hassles and headaches of being an early adopter with payments processing technology that you may not have the resources to develop and scale throughout your business, go with someone like Abtek.

• Meanwhile, the Electronic Transactions Association, has blasted the CurrentC technology as being anti-consumer and anti-competitive.

Want to learn more? Stay up-to-date with breaking news by following us on Facebook and Twitter.Â

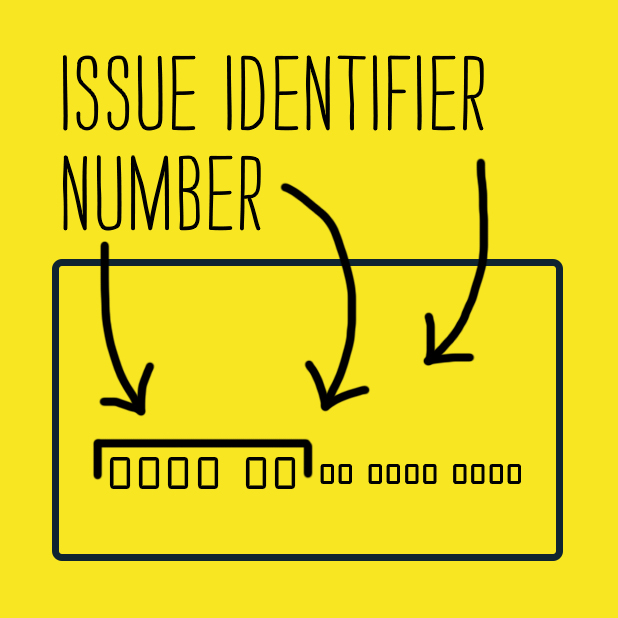

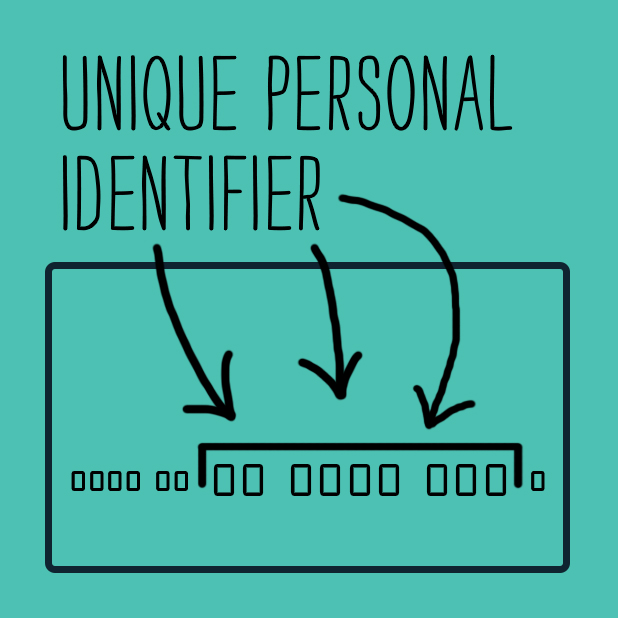

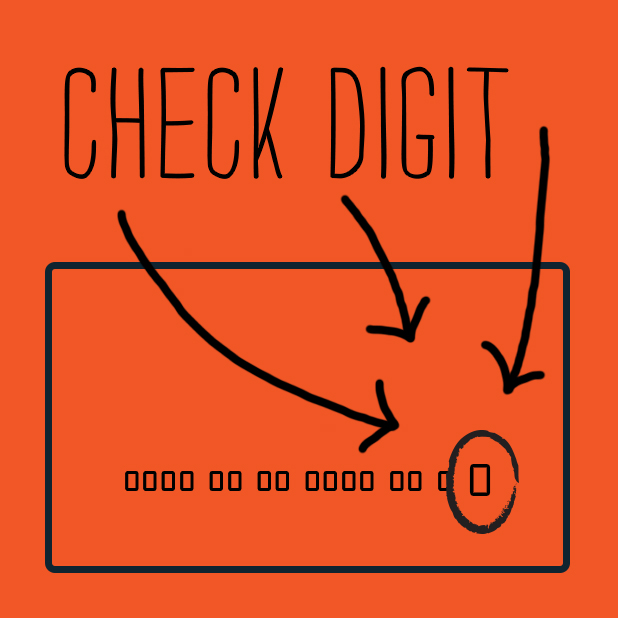

If you’ve ever had to manually key a credit card number into an automated phone system, you’ve probably wondered why the number is so long. Actually, each digit in a credit card number is important for validation, security and identification during credit card processing. Take a moment to learn what each of these digits means.

If you’ve ever had to manually key a credit card number into an automated phone system, you’ve probably wondered why the number is so long. Actually, each digit in a credit card number is important for validation, security and identification during credit card processing. Take a moment to learn what each of these digits means.

In some cases, the system might request a PIN number, but this is usually only for very large purchases or in cases where the automated system detects unusual payment activity for a specific customer.

In some cases, the system might request a PIN number, but this is usually only for very large purchases or in cases where the automated system detects unusual payment activity for a specific customer.